When you hear "ACA plan," you might think of a generic health insurance policy with vague benefits. But the Affordable Care Act isn’t just another insurance option-it’s a system with real rules, clear protections, and specific financial help that can cut your monthly bill by more than half. If you’re shopping for coverage on HealthCare.gov or your state’s exchange, you need to know exactly what you’re getting. This isn’t about theory. It’s about what shows up on your card, what gets covered when you need it, and how much you’ll actually pay out of pocket.

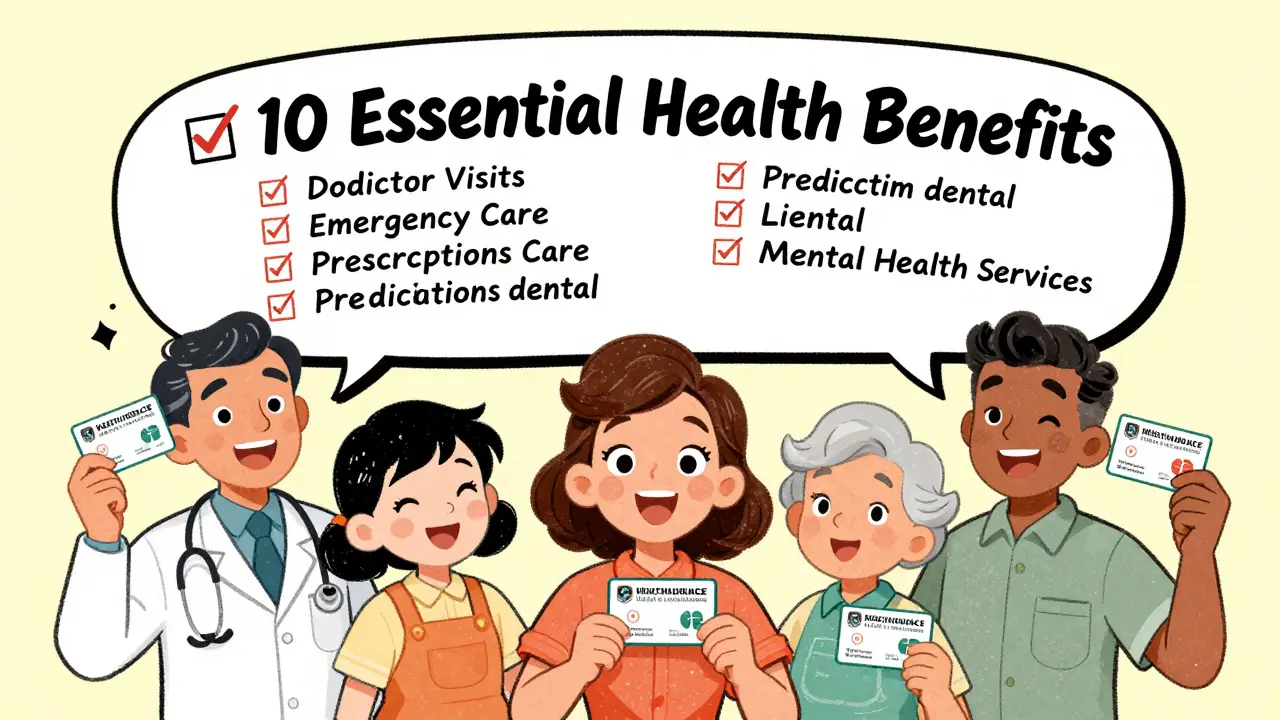

What’s Covered? The 10 Essential Health Benefits

Every ACA plan, whether it’s Bronze, Silver, Gold, or Platinum, must include the same 10 essential health benefits. No exceptions. No fine print tricks. These aren’t optional add-ons-they’re the baseline. That means if you buy a plan, you’re guaranteed coverage for:

- Ambulatory patient services (doctor visits, outpatient care)

- Emergency services

- Hospitalization (like surgery or overnight stays)

- Pregnancy, maternity, and newborn care

- Mental health and substance use disorder services

- Prescription drugs

- Rehabilitative and habilitative services (physical therapy, speech therapy)

- Laboratory services

- Preventive and wellness services (vaccines, screenings, annual checkups)

- Pediatric services (including dental and vision for kids)

That last one matters. Before the ACA, many plans didn’t cover kids’ dental care at all. Now, if you have a child on your plan, their checkups, cleanings, and even orthodontics (in some cases) are included. This isn’t a perk. It’s the law.

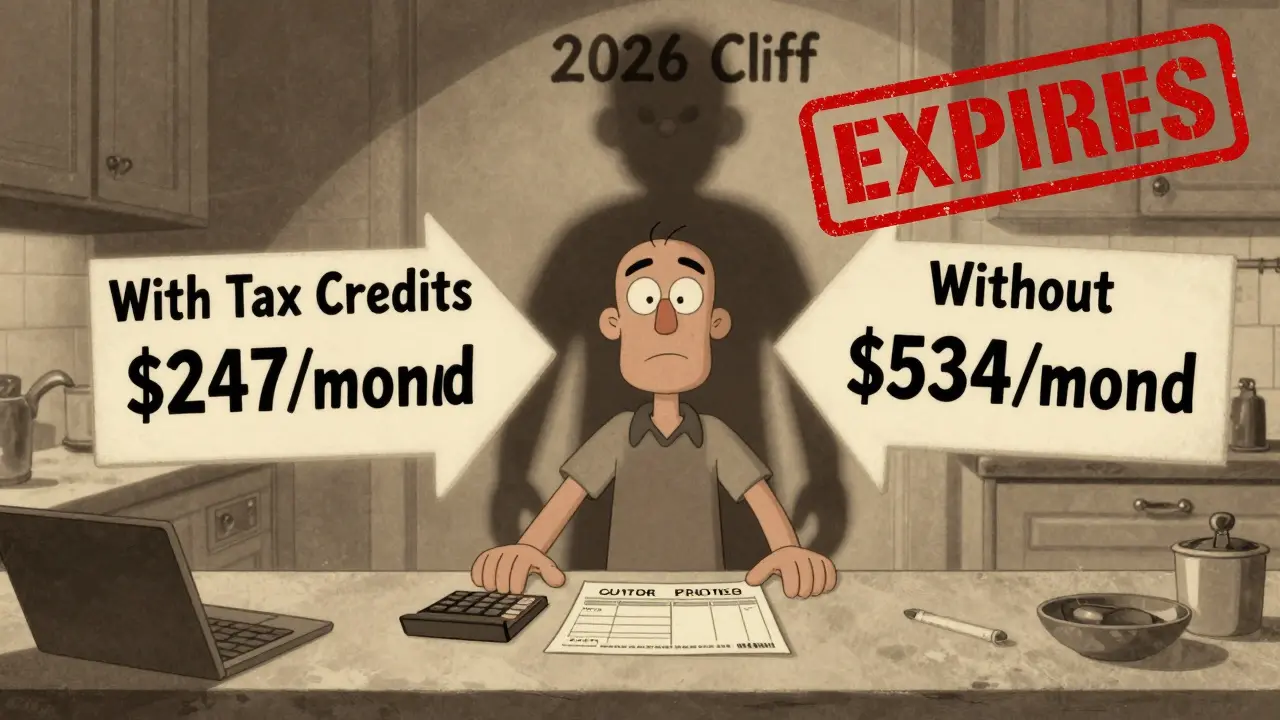

How Premium Tax Credits Actually Work (And Why They’re Disappearing)

The biggest reason people choose ACA plans isn’t the coverage-it’s the cost. And the cost is slashed by something called premium tax credits. These aren’t refunds. They’re upfront discounts that lower your monthly bill. For example, a 40-year-old making $50,000 a year in 2025 pays about $247 a month for a Silver plan with tax credits. Without them? $534. That’s a $287 monthly savings. That’s more than a car payment.

But here’s the problem: those enhanced credits were never meant to last. They were temporary fixes from the American Rescue Plan (2021) and extended by the Inflation Reduction Act (2022). They expire at the end of 2025. Without action from Congress, the average monthly premium will jump by $1,016 per person. For someone over 60, the increase could hit 192% in some states. That’s not a tweak. That’s a financial shock.

Who gets hit hardest? People just above the Medicaid cutoff. In states that expanded Medicaid, you’re covered if you earn under 138% of the Federal Poverty Level. But if you make $1,000 more than that? You’re suddenly in the Marketplace. And if your income bumps up even slightly-say, from $55,000 to $57,000-you could lose your subsidy entirely. That’s called the "cliff effect." One extra paycheck, and your insurance doubles.

Why Your Plan’s Metal Tier Isn’t Just a Label

You’ve probably seen Bronze, Silver, Gold, Platinum. But most people think it’s just about "how good" the plan is. It’s not. It’s about how much you pay vs. how much the plan pays.

Here’s the breakdown:

- Bronze: 60% covered by plan, 40% you pay. Lowest premiums, highest out-of-pocket costs. Best for healthy people who rarely go to the doctor.

- Silver: 70% covered. This is the one that unlocks cost-sharing reductions (CSRs) if you earn under 250% of the poverty level. That means lower deductibles and copays. Many people on subsidies pick Silver because it’s the only tier that gives extra savings.

- Gold: 80% covered. Higher premiums, but you pay less when you need care. Good for people with chronic conditions or frequent prescriptions.

- Platinum: 90% covered. Highest premiums, lowest out-of-pocket. Only makes sense if you’re in and out of the hospital regularly.

Here’s the catch: if you earn between 100% and 250% of the poverty level, choosing Silver isn’t just smart-it’s essential. You get both premium tax credits and cost-sharing reductions. That means your deductible might drop from $7,000 to $1,500. That’s not a discount. That’s life-changing.

What’s Not Covered? The Hidden Gaps

ACA plans cover a lot-but not everything. And some of the gaps are dangerous if you don’t know about them.

First, dental and vision for adults. Only pediatric dental is required. If you’re 35 and need braces or a root canal? That’s on you. Some plans offer optional dental riders, but they’re expensive.

Second, long-term care. If you need help with daily tasks-bathing, dressing, eating-after a stroke or injury, Medicare won’t cover it, and neither will your ACA plan. That’s a $7,000-a-month expense. No insurance helps.

Third, out-of-network care. Even if you pick a Gold plan, your network might be tiny. A 2025 CMS survey found 68% of enrollees in rural areas had fewer than 3 specialists within 50 miles. If your doctor isn’t in-network? You pay full price. No negotiation. No discount.

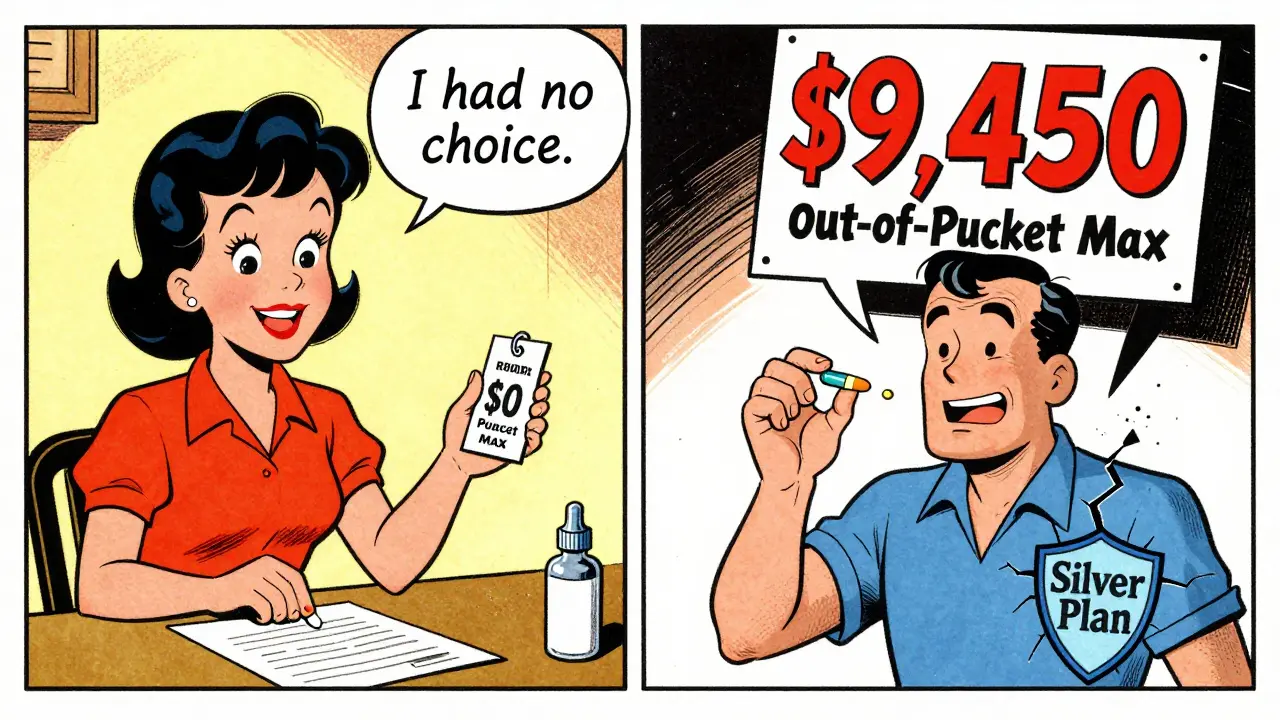

And here’s the kicker: ACA plans have annual out-of-pocket maximums of $9,450 for individuals in 2025. That’s $1,150 more than Medicare Advantage plans. So if you get seriously ill, you could still owe thousands-even with a Silver plan.

Who Qualifies? The Rules Are Changing

You might think anyone can sign up. Not anymore. The CMS 2025 Final Rule, effective November 2025, made major changes:

- DACA recipients are no longer eligible. About 550,000 people will lose coverage by 2026.

- Monthly Special Enrollment Periods for people under 150% FPL are gone. You can only enroll during Open Enrollment or after a qualifying life event (marriage, birth, job loss).

- Income verification now requires direct IRS data matching. No more self-reported numbers.

That last one sounds good-it’s supposed to stop fraud. But it’s also slowing things down. The average application now takes 45 minutes. For self-employed people? You need 6 to 8 hours of prep. You need W-2s, 1099s, bank statements, and proof of business expenses. One mistake, and your subsidy vanishes.

And if your income changes mid-year? Tough luck. You can’t adjust your subsidy until tax season. A Reddit user from Texas, u/ACA_Warrior, posted in August 2025: "My income dropped 30% mid-year. I had to pay $2,800 in medical bills because I couldn’t update my subsidy. Then I got a tax bill for $3,200." That’s the system right now.

Real Stories, Real Costs

Sarah K., a freelance writer in Ohio, earns $32,000 a year. She’s on a Silver plan. With tax credits, her premium is $0. Her deductible is $500. She pays $10 for a doctor visit. $15 for a generic drug. She’s never had a surprise bill. "I thought I’d have to choose between food and meds," she says. "Now I just go to the doctor."

But then there’s James, 58, from Florida. He earns $58,000. He qualifies for a Gold plan, but his subsidy is tiny. He pays $410 a month. His out-of-pocket max is $9,450. He has diabetes. He takes three prescriptions. Last year, he hit his max in October. He stopped filling his insulin for six weeks. "I didn’t have a choice," he says. "I’m not poor. But I’m not covered."

That’s the split. One person gets near-free care. Another gets a plan that’s just barely better than nothing.

What Comes Next? The 2026 Cliff

If nothing changes, 2026 will be a disaster. The enhanced tax credits expire. Premiums jump. Enrollment drops. Experts at the Urban Institute estimate a 25-35% premium increase in the first year. The Kaiser Family Foundation predicts a 15-20% drop in enrollment. In states that didn’t expand Medicaid, 42% of enrollees will face premium hikes over 150%.

And here’s the worst part: the people who need help the most-older adults, low-income workers, those with chronic illness-will be hit hardest. Younger, healthier people might drop out. That means fewer healthy people in the pool. That means higher costs for everyone left.

There’s no magic fix. But if you’re on an ACA plan right now, here’s what you can do:

- Know your income. If it’s between 100% and 400% of the poverty level, you qualify for help. Use the HealthCare.gov calculator.

- Choose Silver if you’re under 250% FPL. It’s the only tier with extra savings.

- Keep records. Track every dollar you spend on medical care. You’ll need it for tax season.

- Don’t assume your plan won’t change. Networks shrink. premiums rise. Benefits shift. Review your plan every year.

The ACA didn’t fix healthcare. But it gave millions of people something they didn’t have before: a chance. Not perfection. Not cheapness. Just a shot. And that shot is vanishing.

Do ACA plans cover pre-existing conditions?

Yes. Since 2014, no ACA plan can deny coverage or charge more because of a pre-existing condition like diabetes, cancer, or asthma. This is one of the most important protections in the law. It applies to every plan sold on or off the Marketplace.

Can I keep my current doctor on an ACA plan?

Maybe. ACA plans have provider networks, and they’re often narrower than employer plans. Before enrolling, check if your doctor is in-network. A 2025 CMS survey found that 32% of enrollees discovered their doctor wasn’t covered after signing up. Always verify with your provider directly-don’t trust the insurer’s website.

What happens if my income changes during the year?

You can’t update your subsidy mid-year unless you have a qualifying life event (job loss, marriage, birth). If your income drops, you’ll pay more out of pocket until tax season. If it goes up, you might owe money back when you file taxes. The CMS 2025 Final Rule will require quarterly income updates starting in 2026, which should reduce surprises-but for now, you’re on your own.

Are ACA plans cheaper than employer insurance?

For some people, yes. If you’re self-employed or work for a small business that doesn’t offer coverage, ACA plans with tax credits are often cheaper than buying insurance on your own. But if your employer offers affordable coverage (under 9.12% of your income), you’re not eligible for subsidies. The "family glitch" fix in 2023 changed that for spouses and kids-but not for the employee.

Do ACA plans cover mental health services?

Yes. All ACA plans must cover mental health and substance use disorder services, including therapy, counseling, and inpatient treatment. They must provide this coverage at the same level as physical health services (parity law). But many plans limit the number of sessions. Always check your plan’s mental health benefits before choosing.

11 Comments

Ugh, I just got hit with a $1,200 bill last month for a stupid ear infection. I’m on a Silver plan. They said it was covered. Turns out the doctor was ‘out-of-network’ even though his office is right next to the hospital. How is that legal? I’m done with this mess.

Oh wow, so the ACA is ‘life-changing’ for people who don’t make enough to be poor but too much to be helped? Classic. The system doesn’t care if you’re one paycheck away from disaster-it just wants you to fill out 17 forms and pray to the IRS. I’ve seen people cry over tax forms. This isn’t healthcare. It’s a financial obstacle course with a Band-Aid labeled ‘affordable.’

you know what they dont tell you? the gov is using your data to track your spending. they cross-check your bank accounts with your ‘income’ and if you spent $500 on a vacation? suddenly you ‘overreported’ and owe $4k. i heard this from a guy on a forum. he lost his subsidy because he bought a $300 plane ticket to visit his mom. its all a scam. the real goal is to make you poor so they can take over.

Let’s be real: Silver plans are a trap. You think you’re getting ‘extra savings’? Nah. You’re getting a deductible that still leaves you broke. And don’t even get me started on the ‘cliff effect.’ One extra hour of overtime and BAM-you’re paying $300 more a month. This isn’t policy. It’s psychological warfare on working-class people. And they call it ‘help.’

My mom had to stop her chemo last year because her subsidy vanished after she got a $2k bonus. 😭 She’s 62. She works part-time at Walmart. They told her to ‘wait until tax season.’ I cried for three days. This system is designed to break people. 🤕💔

ACA? More like Always Costing Americans. You think you’re getting ‘essential benefits’? Try getting a dentist to accept it. Try getting a therapist who isn’t booked for 6 months. Try getting insulin without selling a kidney. This isn’t healthcare-it’s a luxury for the lucky few. The rest of us? We’re just collateral damage in a rigged game.

I just want to say how proud I am of the ACA for giving people like Sarah a real shot. 🙌 It’s not perfect, but it’s something. And honestly? That’s more than we had 15 years ago. I know it’s frustrating, but don’t give up on it. We need to fight for it-not tear it down. You’re not alone. We’re all in this together. 💛

Subsidies are just welfare in disguise. If you can’t afford insurance without government handouts, you shouldn’t be buying it. The market should decide. Stop pretending this is ‘healthcare reform.’ It’s redistribution with a pretty website.

Network adequacy metrics are fundamentally flawed. Rural enrollees face structural access deficits due to provider concentration asymmetries. The 68% statistic is misleading-it doesn’t account for telehealth penetration or tiered reimbursement models. We need policy recalibration, not emotional appeals.

I read this whole thing and just… cried. Not because I’m mad. Because I know Sarah. I know James. I’ve been both. I’m a nurse. I’ve watched people choose between insulin and rent. The ACA didn’t fix healthcare. But it gave us a flicker. And right now? That flicker’s about to go out. Please don’t look away.

Wait, so you actually think the government’s going to fix this? 😂 You really believe they’ll extend the credits? They’ve been dragging their feet for years. If you’re not already on a Silver plan with CSR, you’re already behind. I’m switching to catastrophic and praying I don’t get sick. That’s the new strategy.

Write a comment