Most people assume pharmacies make the most money from expensive brand-name drugs. After all, those prescriptions cost hundreds or even thousands of dollars. But the real profit story is hidden in the cheap pills you pick up for $5 at your local drugstore. Generics - the low-cost copies of brand-name drugs - are the hidden engine behind pharmacy profitability. And here’s the twist: pharmacies earn nearly all their profit from these inexpensive drugs, even though they make up only a quarter of total drug spending.

Why Generics Are the Profit Powerhouse

In the U.S., about 90% of all prescriptions filled are for generic drugs. Yet, they account for just 25% of total drug spending. Why? Because brand-name drugs cost so much more. A single monthly supply of a brand-name drug might cost $800. The generic version? $15. But here’s where it gets counterintuitive: pharmacies make far more profit per prescription on the $15 generic than on the $800 brand.

According to data from the Schaeffer Center, pharmacies earn an average gross margin of 42.7% on generic drugs. That means for every $100 in revenue from a generic prescription, the pharmacy keeps about $43 before paying rent, staff, and utilities. For brand-name drugs? That margin drops to just 3.5%. So even though brand drugs bring in more total revenue, the profit per pill is tiny. Generics, despite their low price, are where the real money is made - if you can get paid properly.

The Hidden Cost: How PBMs Squeeze Pharmacies

But here’s the catch: that 42.7% gross margin doesn’t end up in the pharmacy owner’s pocket. It gets eaten up by pharmacy benefit managers (PBMs) - the middlemen between insurers, pharmacies, and drug manufacturers. PBMs negotiate reimbursement rates with pharmacies, but they don’t always pay what they promise.

One common practice is called spread pricing. The PBM tells the insurance company it’s paying $12 for a generic drug, but only reimburses the pharmacy $8. The $4 difference? That’s the PBM’s profit. The pharmacy gets stuck with the bill for rent, staff, and inventory, while the PBM pockets the spread. In some cases, pharmacies are paid less than what they paid for the drug - a practice known as a clawback. That means the pharmacy loses money on every prescription, even if it’s a generic.

A 2022 survey by the National Community Pharmacists Association found that 68% of independent pharmacy owners ranked declining generic reimbursement as their biggest threat. One owner in Ohio told Pharmacy Times: “My net profit on generics dropped from 8-10% five years ago to barely 2% now. My overhead went up 35%.”

The Consolidation Problem

Three PBMs - CVS Caremark, Express Scripts, and OptumRx - control about 80% of the market. That kind of power lets them set the rules. Independent pharmacies have little leverage. Chains with hundreds of locations can negotiate better terms. But small pharmacies? They’re stuck with whatever rates the PBM offers.

Meanwhile, the generic drug market itself is becoming less competitive. Between 2014 and 2016, nearly 100 mergers happened among generic manufacturers. Today, the top five companies control 45% of the market, up from 32% in 2015. Fewer manufacturers mean less competition - and that leads to price spikes. In some cases, when only one company makes a generic version of a drug, its price can actually rise above the original brand-name version.

Channel Differences: Mail-Order vs. Local Pharmacy

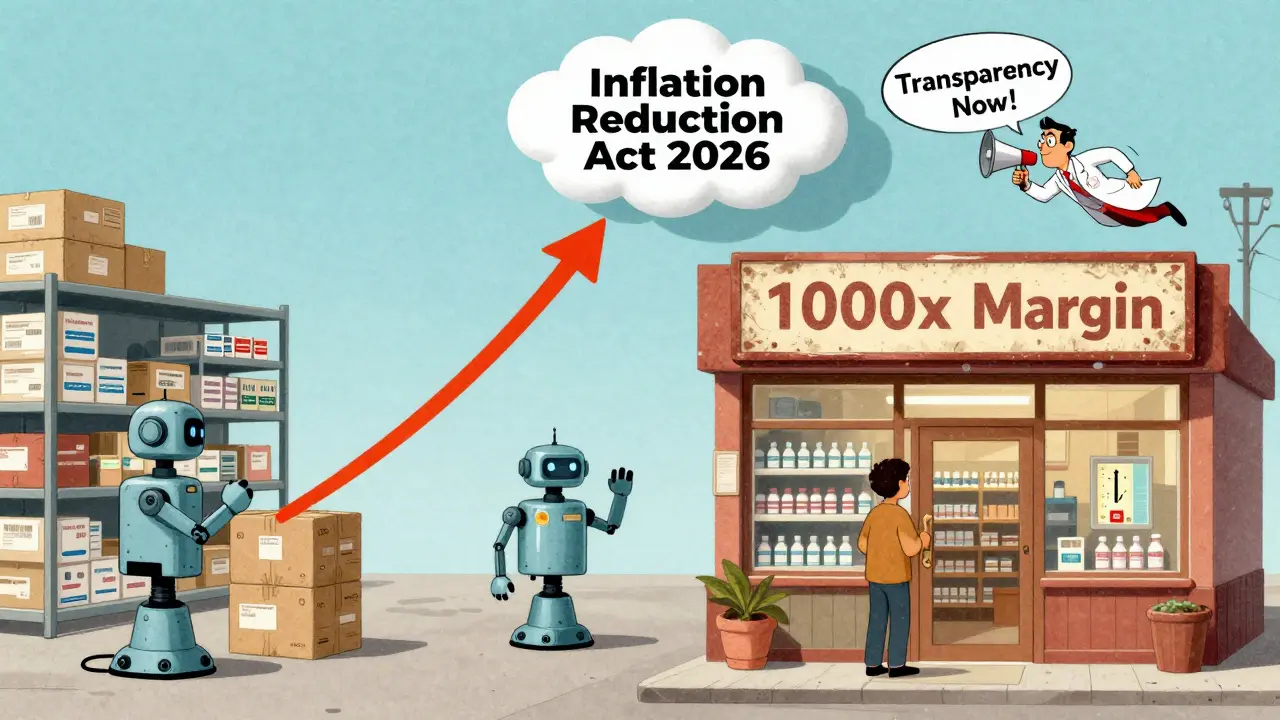

Not all pharmacies are created equal. Mail-order pharmacies, which ship drugs directly to patients, have a huge advantage. Data from 3Axis Advisors shows that for certain generic drugs, mail-order pharmacies make roughly 1,000 times more margin than a local grocery store pharmacy. Why? Because they don’t have the same overhead - no in-store staff, no rent for a storefront, no foot traffic costs. They operate at scale, often with automated systems and bulk purchasing.

On the brand side, the gap is even wider. Mail-order pharmacies make over 35 times more margin on brand drugs than small independent pharmacies. That’s why big insurers push patients toward mail-order - it’s cheaper for them, but it’s killing the local pharmacy business.

What’s Keeping Pharmacies Alive?

Independent pharmacies aren’t giving up. Many are shifting strategies. Some are adding medication therapy management (MTM) services - helping patients manage complex drug regimens for diabetes, high blood pressure, or asthma. These services are reimbursed separately, often by Medicare, and can bring in steady income.

Others are cutting out PBMs entirely. Some pharmacies now offer direct cash-pay pricing. For example, Mark Cuban’s Cost Plus Drug Company charges $20 for a generic drug plus a $3 dispensing fee - no middleman, no mystery. Customers pay upfront, and the pharmacy keeps the full amount. It’s a simple model, and it’s working. As of mid-2024, Cost Plus Drug Company processes over a million prescriptions monthly.

Amazon Pharmacy is another disruptor. It shows clear, upfront pricing - $5 for many generics, with no hidden fees. That’s forcing traditional pharmacies to rethink how they price and communicate value.

What’s Next? Regulatory Pressure and Reform

Regulators are starting to take notice. The Federal Trade Commission has launched investigations into PBM practices and filed antitrust lawsuits against generic manufacturers accused of price-fixing. In 2023, the FTC held a workshop specifically focused on pharmacy reimbursement practices.

States are acting too. California, Texas, and Illinois passed laws in 2022-2023 requiring PBMs to disclose how they calculate reimbursement rates. Transparency is the first step toward fairness.

The Inflation Reduction Act, which begins Medicare drug price negotiations in 2026, may also indirectly affect generic margins. If brand-name drug prices fall, more patients may switch to generics - increasing volume but potentially lowering reimbursement rates further. It’s a double-edged sword.

Still, the long-term outlook is bleak for independent pharmacies. Goldman Sachs predicts 20-25% more closures by 2027 unless reimbursement reforms happen. But there’s hope: pharmacies that diversify into clinical services, adopt transparent pricing, or partner directly with employers are seeing net margins climb to 4-6% - sustainable, but only with real change.

What This Means for You

If you’re a patient: You’re paying more than you think. That $5 generic at the pharmacy? The pharmacy might have paid $3 for it. The rest goes to middlemen, not drugmakers. You might be better off paying cash - especially if you use a service like Cost Plus Drug Company or Amazon Pharmacy.

If you’re a pharmacy owner: Your survival depends on breaking free from PBM dependency. Build direct relationships. Offer clinical services. Be transparent. The old model - waiting for PBMs to pay you fairly - is broken.

If you’re a policymaker: The system is rigged. PBMs, manufacturers, and mail-order chains are making money. Independent pharmacies, the backbone of rural and underserved communities, are being pushed out. Reform isn’t optional - it’s urgent.

Why do pharmacies make more profit on cheap generics than expensive brand drugs?

Pharmacies earn higher percentage markups on generics because their cost is low. A $15 generic might cost the pharmacy $8, so a $7 markup equals a 42% gross margin. A $800 brand drug might cost $770, so a $30 markup equals only a 3.5% margin. Even though the brand drug brings in more revenue, the profit per dollar is tiny. Generics are volume-driven, high-margin items.

What is spread pricing, and how does it hurt pharmacies?

Spread pricing is when a pharmacy benefit manager (PBM) charges a health plan one price for a drug but pays the pharmacy a lower amount. The difference - the “spread” - goes to the PBM as profit. For example, if the PBM charges the insurer $12 for a generic but pays the pharmacy $8, the PBM keeps $4. The pharmacy still has to cover rent, staff, and inventory, so they lose money on the transaction. This practice is common and often hidden from patients and pharmacies.

Why are generic drug prices sometimes higher than brand-name prices?

This happens when only one manufacturer makes a generic version - a situation called a single-source generic. Without competition, that manufacturer can raise prices. In some cases, supply chain issues or manufacturing shutdowns force the market into this state. The FDA has documented cases where single-source generics cost more than the original brand, especially for older drugs with low demand.

Can pharmacies survive without PBMs?

Yes - but it requires a major shift. Some pharmacies now bypass PBMs entirely by offering direct cash pricing, partnering with employers for self-funded plans, or using transparent platforms like Cost Plus Drug Company. These models give pharmacies full control over pricing and eliminate clawbacks and spread pricing. While it takes time and customer education, pharmacies using these methods report 3-5% higher net margins.

What’s the future for independent pharmacies?

Without reform, independent pharmacies face a steep decline. Between 2018 and 2023, 3,000 closed. Goldman Sachs predicts 20-25% more closures by 2027. But pharmacies that add clinical services like medication therapy management, adopt transparent pricing, or form alliances with local health systems can survive - and even thrive. The future belongs to pharmacies that become healthcare providers, not just pill dispensers.

11 Comments

I never realized how much profit pharmacies make on $5 generics. It’s wild that the cheaper the pill, the more they earn. Makes you rethink what 'affordable' even means anymore.

Also, PBMs are basically tax collectors for no reason. Why do we even have them?

Lol u think this is bad? wait till u see how big pharma rips us off. its all a scam. generics are just placebo with labels. 💅

Oh wow so the pharmacy makes more off a $15 generic than a $800 brand? That’s like saying a hot dog stand makes more profit off a $1 bun than a $500 steak.

PBMs are the real villains here. They’re not middlemen - they’re middlemen with a credit card and zero ethics.

I used to work at a small pharmacy. We lost money on every generic script because of clawbacks. It was insane. We’d fill the prescription, get paid $7.50, but the drug cost us $8.20.

My boss cried once. Not dramatic. Just… quiet. And then he kept showing up. We’re all just trying to keep the lights on.

PBMs are why my grandma pays $20 for a $3 pill 😭

I just started using Cost Plus Drug Co. and it’s a game changer. No drama. No surprise fees. Just $20 + $3. I wish more people knew about this.

Also, if you’re a pharmacy owner - stop waiting for PBMs to save you. Build your own thing. It’s scary but worth it. ❤️

Stop pretending this is a healthcare issue. This is a capitalism issue. PBMs are corporate vultures. Pharmacies are collateral damage. Patients are the ones paying the price. Fix the system or shut up.

America is broken. We pay more for medicine than any country. And the worst part? We let it happen. You think PBMs are bad? Wait till you see who owns them. Big banks. Big pharma. Same people who own your TV. This isn’t coincidence. It’s design.

It’s interesting how the system rewards volume over value. A pharmacy that fills 500 generics a day makes more than one that fills 50 expensive scripts. But no one talks about the human cost - the staff, the burnout, the closed storefronts in towns that already had nothing.

Maybe profit isn’t the only metric that matters.

wait so i can just pay cash and get it cheaper? why didnt anyone tell me this sooner lmao

The real tragedy isn’t the PBM spreads or the clawbacks. It’s that we’ve normalized this. We accept that a $5 pill costs $12 because ‘that’s how it works.’ We don’t question the invisible hand - we just hand over our money.

But imagine if pharmacies could set their own prices. Imagine if patients knew what drugs actually cost. Imagine if we treated healthcare like a public good, not a profit center.

It’s not impossible. It just requires us to stop being polite and start being loud.

Write a comment